Media Summary: MIT 18.S096 Topics in Mathematics with Applications in Finance, Fall 2013 View the complete course: ... MIT 18.642 Topics in Mathematics with Applications in Finance, Fall 2024 Instructor: Peter Kempthorne View the complete course: ... Today we are going to talk about uh branching processors this is also one of the branches in

17 Stochastic Processes Ii - Detailed Analysis & Overview

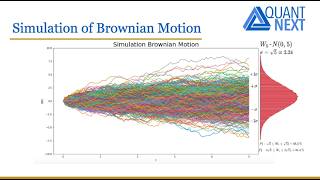

MIT 18.S096 Topics in Mathematics with Applications in Finance, Fall 2013 View the complete course: ... MIT 18.642 Topics in Mathematics with Applications in Finance, Fall 2024 Instructor: Peter Kempthorne View the complete course: ... Today we are going to talk about uh branching processors this is also one of the branches in In this video, I explain Brownian motion (or Wiener process), a fundamental concept in To solve the geometric Brownian motion SDE which is assumed in the Black-Scholes model. welcome friends we will take about the twenty sixth lecture where we will address the